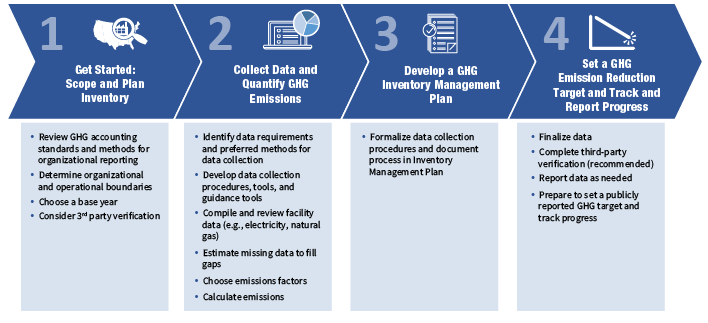

Requirements

Reporting is crucial to ensure accountability and effective engagement with stakeholders. This blog(Requirements) summarizes the various reporting requirements specified in and identifies additional reporting considerations that together provide a credible reporting framework and enable users of reported data to make informed decisions. It is essential that the reported information is based on the key accounting principles (relevance, accuracy, completeness, consistency, and transparency).

Companies shall publicly report the following information to be in conformance with the GHG Protocol Product Standard:

- General information and scope

- Contact information

- Studied product name and description

- The unit of analysis and reference flow

- Type of inventory, cradle-to-grave or cradle-to-gate

- Additional GHGs included in the inventory

- Any product rules or sector-specific guidance used

- Inventory date and version

- For subsequent inventories, a link to previous inventory reports and description of any methodological changes

- A disclaimer stating the limitations of various potential uses of the report including product comparison

- Boundary setting

- Life cycle stage definitions and descriptions

- A process map including attributable processes in the inventory

- Non-attributable processes included in the inventory

- Excluded attributable processes and justification for their exclusion

- Justification of a cradle-to-gate boundary, when applicable

- The time period

- The method use to calculate land-use change impacts, when applicable

- Allocation

- Disclosure and justification of the methods used to avoid or perform allocation due to coproducts or recycling

- When using the closed loop approximation method, any displaced emissions and removals separately from the end-of-life stage

- Data collection and quality

- For significant processes, a descriptive statement on the data sources, data quality, and any efforts taken to improve data quality

- Uncertainty

- A qualitative statement on inventory uncertainty and methodological choices. Methodological choices include:

- Use and end-of-life profile

- Allocation methods, including allocation due to recycling

- Source of global warming potential (GWP) factors used

- Calculation models

- Inventory results

- The source and date of the GWP factors used

- Total inventory results in units of CO2e per unit of analysis, which includes all emissions and removals included in the boundary from biogenic sources, non-biogenic sources, and land-use change impacts

- Percentage of total inventory results by life cycle stage

- Biogenic and non-biogenic emissions and removals separately when applicable

- Land use impacts separately when applicable

- Cradle-to-gate and gate-to-gate inventory results separately (or a clear statement that confidentiality is a limitation to providing this information)

- The amount of carbon contained in the product or its components that is not released to the atmosphere during waste treatment, when applicable

- For cradle-to-gate inventories, the amount of carbon contained in the intermediate product

- Assurance:

The assurance statement including:

- Whether the assurance was performed by a first or third party

- Level of assurance achieved (limited or reasonable) and assurance opinion or the critical review findings

- A summary of the assurance process

- The relevant competencies of the assurance providers

- An explanation of how any potential conflicts of interest were avoided for first party assurance

- Setting reduction targets and tracking inventory changes:

Companies that report a reduction target and/or track performance over time shall report the following:

- The base inventory and current inventory results in the updated inventory report

- The reduction target, if established

- Changes made to the inventory, if the base inventory was recalculated

- The threshold used to determine when recalculation is needed

- Appropriate context identifying and describing significant changes that trigger base inventory recalculation

- The change in inventory results as a percentage change over time between the two inventories on the unit of analysis basis

- An explanation of the steps taken to reduce emissions based on the inventory results.