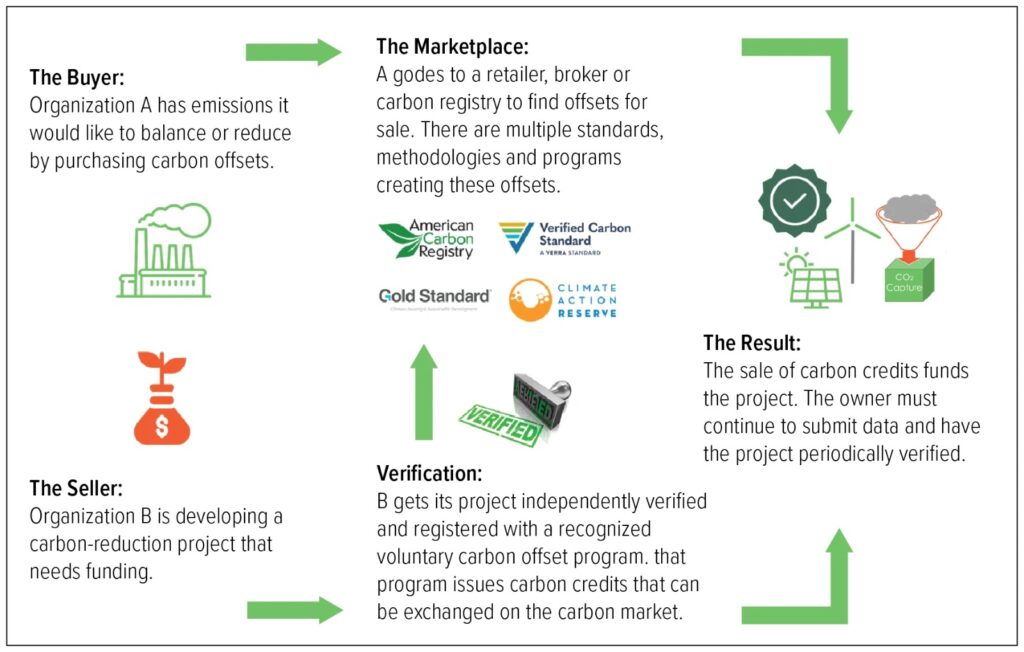

Voluntary carbon offsets play a role in assisting companies and nations in achieving their ambitious climate goals. Through the purchase of “Credits” from initiatives that either decrease or eliminate carbon emissions, both private businesses and government bodies aim to decrease the effects of their emissions in the near future, while simultaneously striving to eventually eliminate their carbon footprint.

CO2 reduction targets

In order to achieve the sustainability objectives outlined in the 2015 Paris Climate Agreement, along with the diverse targets set by different countries and businesses, research suggests that the global community needs to eliminate a minimum of 1 gigaton of carbon dioxide annually by 2030. This assessment is based on the evaluation of information from the Network for Greening the Financial System. However, it’s worth noting that the potential for credits related to avoidance or reduction is much greater, potentially reaching up to 10 gigatons annually. Each individual carbon offset stands for one metric ton of carbon dioxide that has been removed from, decreased in, or prevented from entering the atmosphere.

Statistics and thoughts

“The market for carbon offsets has undergone rapid transformation, generating heightened interest from investors and corporations,” explains Carolyn L. Campbell, who leads ESG fixed income research. While carbon offsets should ideally be employed solely to counter emissions that cannot be avoided and lack viable alternatives, they provide a crucial pathway while alternative decarbonization methods are developed. According to Campbell and her team’s assessment, approximately 4,000 carbon-offset projects have issued credits, resulting in roughly 1.7 billion offsets removed (equivalent to 1.7 gigatons of carbon). With another 3,800 projects either listed, pre-registered, or registered and awaiting credit issuance, the voluntary carbon-offsets market is poised to expand from approximately $2 billion in 2022 to an estimated $100 billion by 2030, and further to around $250 billion by 2050.

However, the specific areas where this expansion takes place are primarily influenced by three significant changes within the carbon offset market. These changes revolve around the selection of credits to acquire and the decision of whether to engage in purchasing at all. Within this context, this blog delves into the potential risks, avenues for growth, and emerging patterns.

Transitioning: From Reducing and Avoiding to Direct Removal

At present, a dominant 82% share of the offsets market is occupied by projects that prioritize evading or lessening carbon dioxide emissions in the atmosphere. Those opting for these types of offsets gain acknowledgment for averting potential emissions, such as safeguarding forests or adopting renewable energy alternatives over fossil fuels.

In contrast, removal credits, constituting a modest 5% of the market, address the ramifications of past emissions. These credits originate from initiatives that actively extract carbon dioxide from the atmosphere, like planting trees for carbon sequestration or employing technology-driven methods to directly capture carbon from industrial operations and fossil fuel-based power plants. (The remaining 13% accounts for a blend of avoidance/reduction and removal projects.)

While the significance of removal projects is anticipated to grow in the long run, present obstacles related to scaling and costs limit their availability. In the interim, avoidance and reduction credits will continue to bridge the gap until the transition is fully realized.

Carolyn L. Campbell notes, “Avoidance credits remain pertinent currently and can finance crucial shifts in anticipation of regulations, legislation, or economic viability.”

As the trajectory of the decade unfolds, and the focus shifts towards removal projects that definitively and permanently extract carbon dioxide from the atmosphere, the accumulation of carbon-offset credits should suffice to meet companies’ net-zero aspirations.

Transitioning: From Natural Solutions to Technological Innovations

Projects centered around nature-based carbon offsets predominantly target the reduction of emissions through actions like halting deforestation and curbing forest degradation. Although measuring their impact proves challenging, these projects constitute a vital interim solution until all available land is reforested or until nations enact more stringent regulations for conserving existing forests and natural ecosystems.

However, moving beyond 2030, it’s probable that technology-driven carbon removal efforts will surpass nature-based approaches. Carolyn L. Campbell notes, “In fact, many established net-zero models anticipate a reliance on technology-based removals after 2030, with projections of over 5 gigatons of carbon dioxide removed annually by 2050.”

Technological offset projects encompass a variety of measures, including the adoption of new renewable technologies, the prevention or capture of methane leaks from activities like fossil fuel production, mining, landfills, or livestock, the substitution of wood-burning stoves with clean alternatives, direct capture of carbon dioxide from the atmosphere, and the secure storage of captured carbon from emission sources underground for permanent sequestration.

Transitioning: Shifting from Offsets to Strategic Investments

In an ideal scenario, a company or nation should allocate resources to adopt technologies, enhancements, and efficiencies that lead to achieving absolute zero emissions. Meanwhile, during the transitional period, it’s beneficial to offset current emissions. Notably, specific industries such as airlines are increasingly diverting a larger portion of their sustainability budgets to research and development, moving away from offset purchases. This shift is particularly evident among air carriers, who, governed by sector-specific decarbonization regulations and holding significant control over their emissions, have a unique opportunity to invest in available, albeit costly and evolving, technological solutions that align with their decarbonization objectives. While the steel and cement sectors, also heavy emitters, share similar characteristics, they aren’t bound by global emissions mandates like airlines and lack the same direct connection with end consumers.

Conclusion

In summary, the trajectory of the voluntary carbon offset market points toward a substantial upsurge in the years to come. This surge is not merely a numerical shift, but a testament to the growing awareness and commitment to address the environmental challenges of our time. As individuals, companies, and nations embrace the importance of carbon mitigation, the voluntary carbon offset market offers a vital avenue for contributing to a sustainable future. With the anticipated rise in removal projects, technological innovations, and a renewed focus on reducing emissions, the market’s potential to effect positive change is substantial. As we embark on this transformative journey, the collective efforts of diverse stakeholders will play a crucial role in propelling the voluntary carbon offset market forward, further solidifying its role in shaping a more environmentally responsible and resilient world.