Understanding the EU Carbon Border Adjustment Mechanism (CBAM) and Its Implications for India

May 28, 2025

Introduction:

The European Union’s Carbon Border Adjustment Mechanism (CBAM) is a pioneering climate policy tool that reflects the EU’s commitment to achieving climate neutrality by 2050. By placing a carbon price on certain imports, CBAM seeks to prevent “carbon leakage”—a phenomenon where companies move production to countries with less stringent emissions rules—and ensure that climate efforts within the EU are not undermined by foreign competitors. This comprehensive article explains the full scope of CBAM, its implementation roadmap, its technical and practical dimensions, and what it means for India and other developing economies.

What is CBAM?

CBAM is a carbon pricing mechanism that targets imports of carbon-intensive goods into the EU. It complements the EU Emissions Trading System (ETS), which already places a carbon price on domestic producers. Without CBAM, EU industries would face unfair competition from imports produced in countries with looser climate regulations.

Key Objectives:

Level the playing field between EU and non-EU producers

Encourage cleaner production practices globally

Protect EU industries from carbon leakage

Strengthen the EU’s global climate leadership

How it Works:

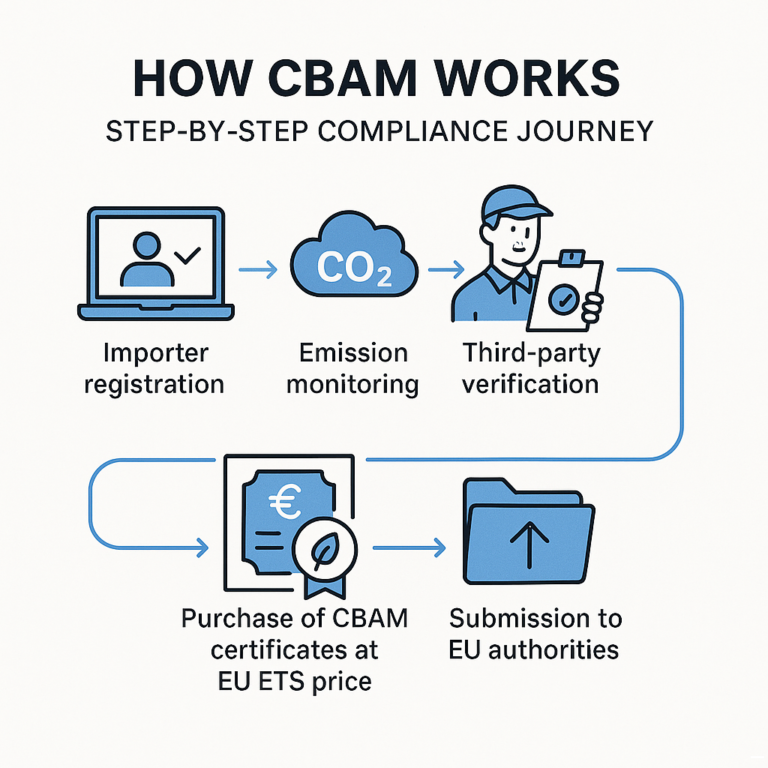

Importers of CBAM-covered goods will need to:

Calculate the embedded CO₂ emissions of their products

Submit verified emissions reports

Purchase and surrender CBAM certificates equivalent to those emissions, priced at the EU ETS rate

The mechanism began with a transitional phase in October 2023 and will be fully enforced from January 2026.

Full Scope of CBAM (Post-2026)

Initially, CBAM focuses on a limited number of highly polluting sectors, but the regulation is designed to expand its coverage over time. As of 2026, the following goods will fall within its scope:

Core Sectors Covered:

Iron and Steel: Includes semi-finished and selected finished products (e.g., slabs, coils, tubes)

Aluminium: Unwrought and wrought aluminium products

Cement: Clinker and various cement forms

Fertilisers: Products such as urea, ammonium nitrate, and ammonia

Electricity: Imports of electricity from non-EU countries

Hydrogen: Specifically gaseous hydrogen, including grey hydrogen

Future Expansion (Post-Review in 2026)

The EU plans to explore expanding CBAM’s coverage to include:

Downstream products (e.g., screws, pipes, auto parts made from steel or aluminium)

Organic chemicals and polymers

Indirect emissions (emissions from electricity used during production)

Other high-risk sectors, depending on decarbonisation trends and carbon leakage risks

Compliance and Technical Implementation

Transitional Phase (2023–2025):

Importers submit quarterly reports on embedded emissions

No financial penalties or certificate purchases during this phase

Helps businesses prepare for full compliance in 2026

From 2026 Onward:

Importers must register as “authorised CBAM declarants”

Annual reporting of embedded direct emissions, verified by independent third parties

Purchase CBAM certificates at the weekly EU ETS average price

Keep supporting documentation for up to four years

Administrative and Technical Burden: This involves setting up monitoring, reporting, and verification (MRV) systems that align with EU guidelines. Non-compliance may lead to penalties or rejection of imports.

Impact on India: Risks and Challenges

Export Dependence: India exports significant volumes of iron, steel, aluminium, and fertilisers to the EU:

Over 27% of India’s aluminium and steel exports go to the EU

These sectors rely heavily on coal-based energy, making their carbon footprints higher

Estimated Cost Impact:

CBAM could result in tariff-equivalent costs of 20–35% for Indian exporters

For steel exports, the cost could be €173.8 per tonne, amounting to 16% of export value

Structural Challenges for India:

Absence of a national carbon pricing mechanism

Lack of standardised MRV infrastructure

High dependency on fossil fuels

MSMEs may struggle to comply due to limited financial and technical capacity

Trade and Diplomatic Concerns: India has criticized CBAM as discriminatory and possibly WTO-inconsistent. However, the EU maintains that CBAM is a climate measure and not a trade barrier.

Opportunities and Strategic Benefits

Policy Momentum:

Accelerated development of a domestic carbon market or ETS

Launch of a green steel certification scheme

Improved focus on clean hydrogen, electrification, and renewables

Technological Shifts:

Promotion of electric arc furnaces (EAFs)

Recycling and scrap-based production

Incentives for low-carbon fertiliser technologies

Market Differentiation:

Early movers can gain preferential access to climate-conscious markets

Potential to leverage green branding and supply chain leadership

Recommendations for Stakeholders

For Indian Industry:

Begin carbon accounting and lifecycle assessments

Upgrade production systems to lower emissions

Work with EU buyers on aligning data and verification standards

For Policymakers:

Finalise India’s carbon credit trading framework

Develop MRV standards aligned with international norms

Provide fiscal support to MSMEs

For Trade Associations and Think Tanks:

Launch awareness campaigns and training programs

Foster EU–India climate tech collaboration

Monitor trade competitiveness impacts

Conclusion

CBAM is more than a trade measure; it signals a shift to climate-conscious global commerce. For India, it brings challenges but also opportunities for green transformation and innovation. Proactive action across industry, policy, and diplomacy is crucial.

F*ckin’ amazing things here. I am very happy to see your post. Thank you so much and i am looking ahead to touch you. Will you please drop me a e-mail?

Wow, wonderful blog layout! How long have you been blogging for? you made blogging look easy. The overall look of your site is magnificent, as well as the content!

F*ckin’ amazing things here. I am very happy to see your post. Thank you so much and i am looking ahead to touch you. Will you please drop me a e-mail?

I like this web site so much, saved to fav.

Wow, wonderful blog layout! How long have you been blogging for? you made blogging look easy. The overall look of your site is magnificent, as well as the content!

I admire your work, thankyou for all the great posts.