.

Greenhouse gas accounting and reporting is like keeping track of how much pollution a company creates and then telling others about it. It helps companies show how they’re doing in terms of reducing their pollution over time. They might do this for different reasons, such as trying to meet pollution reduction targets, dealing with risks and opportunities related to pollution, and meeting the expectations of people who care about the environment.

Here are the steps a company should follow to track and report their progress in reducing pollution over time:

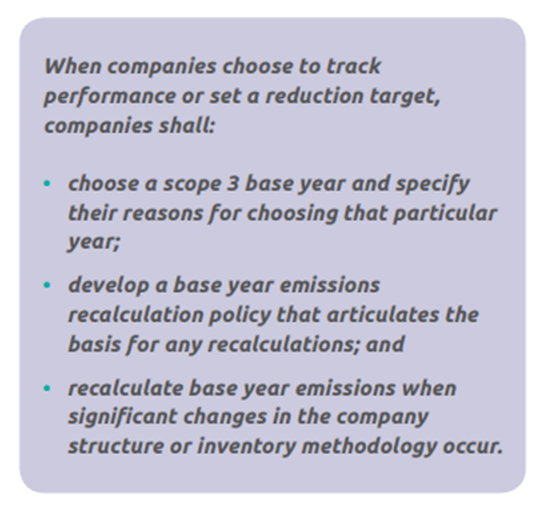

- Choosing a Base Year and Determining Base Year Emissions: First, a company needs to pick a starting year, called the “base year.” This is the year from which they’ll compare their progress. Then, they figure out how much pollution they produced in that base year.

- Setting Scope 3 Reduction Goals: Next, the company decides how much they want to reduce their pollution, and they set specific goals to achieve that reduction. These goals are like targets they want to reach.

- Recalculating Base Year Emissions (if necessary): Sometimes, a company might need to recalculate the pollution from their base year if they find better data or realize they made mistakes before. This helps make sure the starting point is accurate.

- Accounting for Scope 3 Emissions and Reductions Over Time: The company then keeps a record of all the pollution they produce (called emissions) and any pollution they manage to reduce (called reductions) from their day-to-day operations. This is not just pollution from their own activities (Scope 1 and 2), but also from things like their supply chain, transportation, and product use (Scope 3). They keep doing this year after year.

1. Choosing a base year and determining base year emissions

When companies want to measure and compare the pollution they produce over time, they need to pick a starting point, which is called the “base year.” This is like marking the beginning of their efforts to reduce pollution.

Here are the important points explained in detail:

- Choosing a Base Year: To track how well they’re doing in reducing emissions, companies must choose a specific year in the past as a reference point. This year is called the “base year.” It’s like setting a starting line in a race.

- Reasons for Choosing the Base Year: When companies decide on their base year, they need to explain why they picked that particular year. Maybe they had good data for that year, or it’s when they started taking pollution reduction seriously. These reasons help others understand their choice.

- Using the Same Base Year for All Emissions: To make it easier to compare different types of emissions, like those from their own operations (Scope 1 and 2) and those from their supply chain and products (Scope 3), it’s best to use the same base year for all of them. This makes it consistent and comprehensive.

- Choosing a More Recent Base Year for Scope 3: If a company already has a base year for Scope 1 and 2 emissions but wants to start measuring Scope 3 emissions separately, they can pick a more recent year for the Scope 3 base year. This newer year should be the first year with complete and reliable data on Scope 3 emissions.

- When to Set the Scope 3 Base Year: Companies don’t have to set the Scope 3 base year right away. They can wait until they have enough good data for their Scope 3 emissions, which might take a few years. But, once they pick a Scope 3 base year, they must report it.

- Reporting No Base Year Until Chosen: If a company hasn’t decided on a Scope 3 base year yet, they should tell others that they haven’t set one. This shows transparency about their progress.

- Calculating Base Year Emissions: Once the base year is chosen, the company calculates how much pollution they produced in that year. They need to follow specific guidelines and rules outlined in the standard to ensure accuracy.

- Developing a Recalculation Policy: Companies must also create a policy for how they will recalculate emissions from the base year if needed. This ensures that they can update their measurements accurately as they gather more information.

2. Setting scope 3 reduction targets

1. Why Set Greenhouse Gas (GHG) Targets?

Just like a business needs to set goals for things like making money and selling products, it’s important for companies to set targets for reducing their greenhouse gas emissions. This is because managing these emissions is crucial for environmental responsibility. Companies don’t have to set targets specifically for their Scope 3 emissions (emissions related to their supply chain and products), but it’s a good idea to think about it.

2. Different Types of GHG Reduction Goals:

Companies can set various types of targets for reducing emissions:

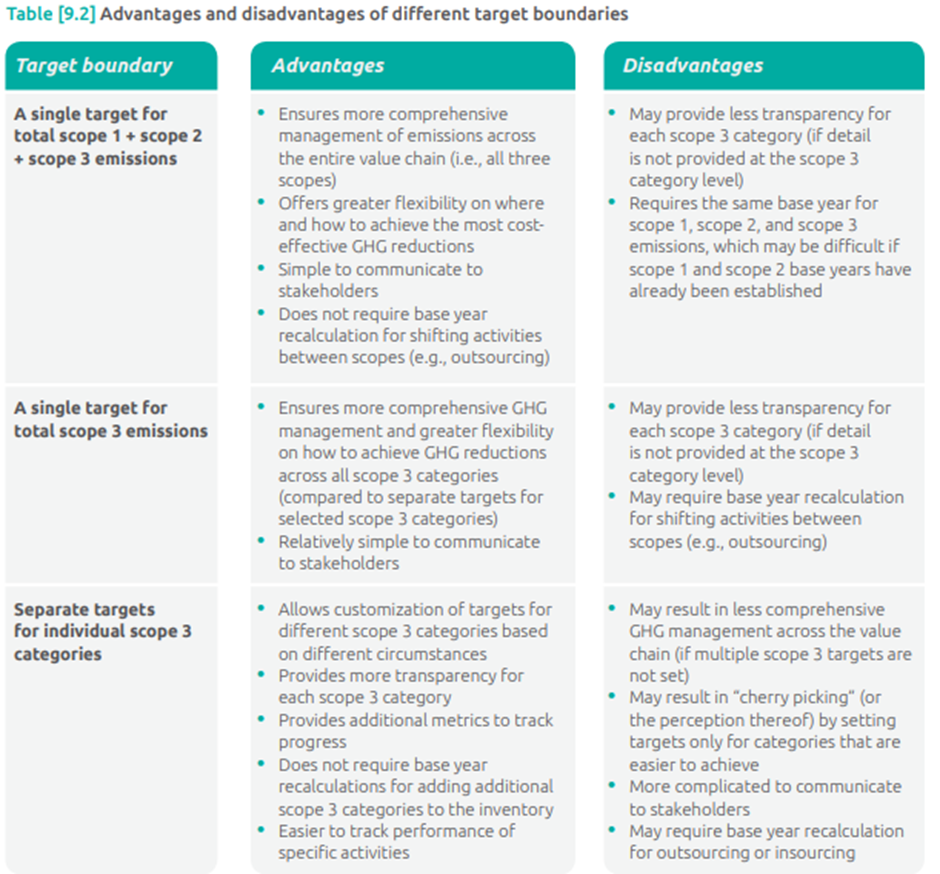

- A single target for all their emissions (Scope 1 + Scope 2 + Scope 3).

- A single target for only their Scope 3 emissions.

- Separate targets for different types of Scope 3 emissions (like transportation or waste).

- A combination of targets, including one for all emissions and separate ones for specific Scope 3 categories.

Each of these target types has its advantages and disadvantages.

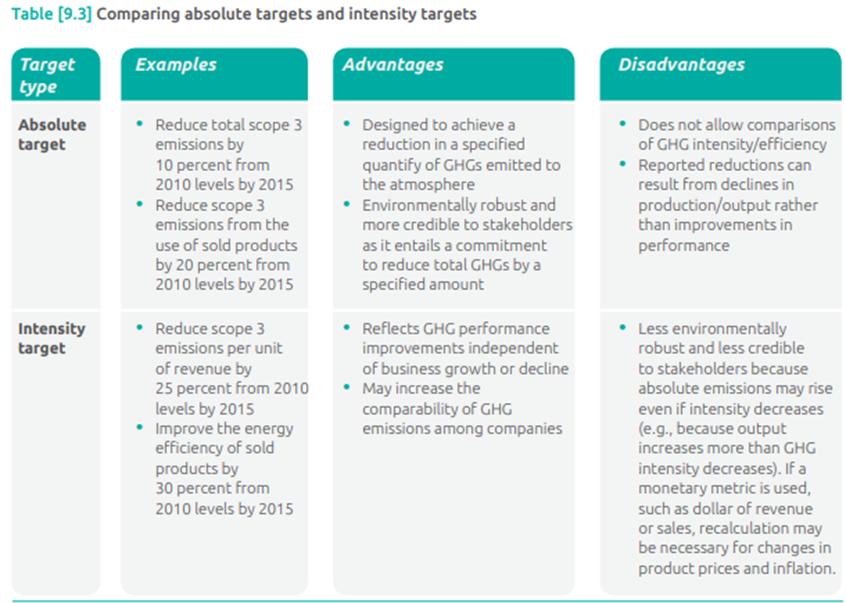

3. Absolute vs. Intensity Targets:

Companies can choose different ways to express their targets.

- An absolute target measures how much they want to reduce emissions in specific units (like metric tons of CO2) over time.

- An intensity target compares emissions to a business metric, like sales or production. It’s expressed as a reduction in emissions relative to that metric.

Companies may find it useful to use both absolute and intensity targets to provide a more comprehensive view of their efforts.

4. Target Completion Date:

Companies should decide when they want to achieve their emission reduction targets. Longer-term targets, like those spanning ten years, are better for planning and investing in eco-friendly practices. Shorter-term targets can help them track progress more frequently.

5. Ambitious Targets:

To set a meaningful target, companies should look at their potential opportunities to reduce emissions and aim for a goal that significantly cuts emissions compared to their usual emissions trajectory. A more challenging target (“stretch goal”) can encourage innovation and gain trust from stakeholders.

6. Use of Offsets:

Companies can meet their GHG targets through two ways:

- Internal reductions within their own operations and supply chain.

- Offsets from projects outside their operations that reduce emissions (like reforestation projects).

Companies should try to meet their targets through internal reductions. If they use offsets, they must be clear about how much of the target was achieved using them. Internal emissions and offset usage should be reported separately.

7. Avoiding Double Counting:

To prevent confusion and ensure the reliability of their emission reductions, companies should follow credible accounting standards for offsets. They should also be careful not to count the same offsets multiple times, especially when multiple parties are involved.