“GHG project accounting” refers to keeping track of greenhouse gas (GHG) emissions from various projects.

Now, when we say “involves making decisions that directly relate to policy choices faced by GHG programs,” it means that while tracking these emissions, certain decisions need to be made. These decisions are connected to the policies set by GHG programs.

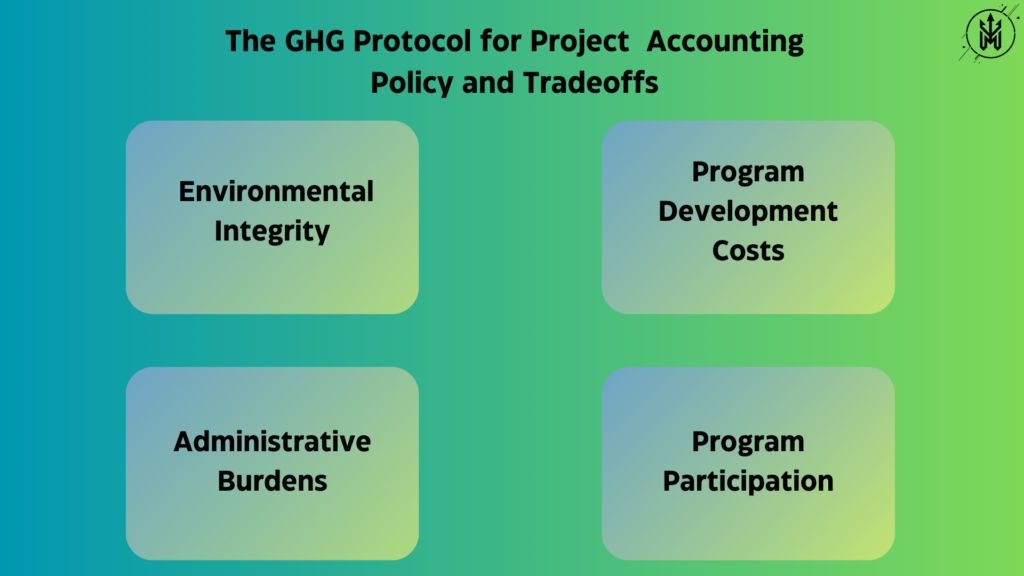

The “policy choices” mentioned involve making tradeoffs. Tradeoffs mean giving up one thing to get something else. In this context, the tradeoffs are between:

- Environmental Integrity: How accurately and effectively the GHG emissions are being measured and reported.

- Program Participation: Encouraging more projects to participate in GHG programs.

- Program Development Costs: The expenses associated with setting up and maintaining the GHG program.

- Administrative Burdens: The workload and complexity of managing the GHG program.

So, the people involved in GHG project accounting need to make decisions that balance these factors. For example, they may need to decide how strict the measurement methods should be (environmental integrity) while considering how this might affect the willingness of projects to participate (program participation) and the overall costs and administrative workload (development costs and administrative burdens).

Additionality

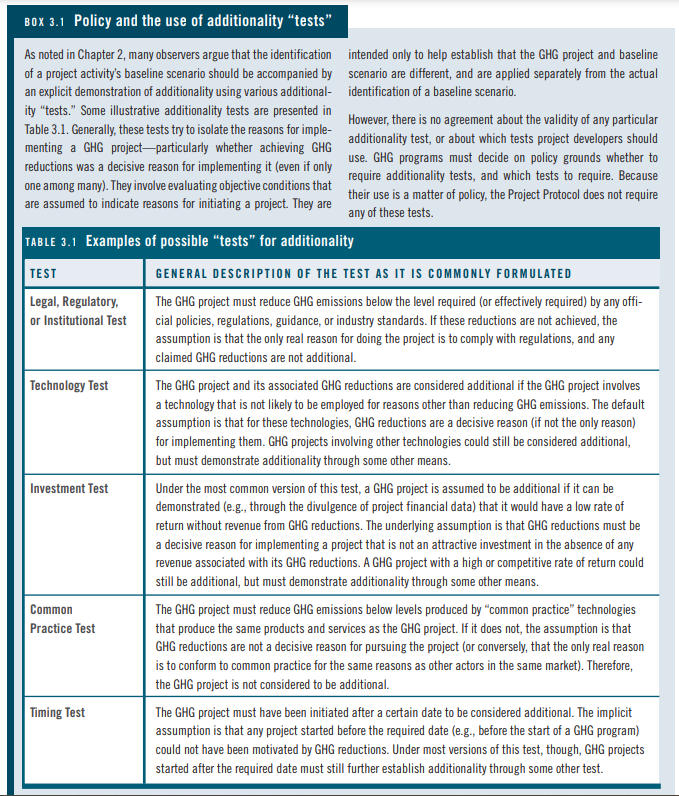

“Additionality” is a crucial concern for programs that deal with reducing greenhouse gas (GHG) emissions. It refers to the idea that the emissions reductions claimed by a project should be additional to what would have happened without the project’s activities.

Now, when it says, “a GHG program must decide how stringent to make its additionality rules and criteria based on its policy objectives,” it means that these programs need to figure out how strict or demanding their rules should be in ensuring that the claimed emissions reductions are truly additional.

There are two main approaches mentioned:

- Project-specific approach: Here, the stringency (strictness) is determined by the amount of evidence needed to identify a specific baseline scenario. The baseline scenario is what would have happened without the project.

- Performance standard approach: In this approach, the stringency is determined by how much better the project’s emissions are compared to the average emissions of similar practices or technologies.

Setting the stringency involves finding a balance. If the criteria are too lenient, they might end up giving credit for emissions reductions that would have happened anyway, which undermines the program’s effectiveness. On the other hand, if the criteria are too strict, they might exclude genuinely additional and desirable projects.

No approach is perfect. Trying to reduce one type of error (e.g., giving credit for non-additional reductions) may increase the likelihood of the other type of error (e.g., rejecting truly additional projects).

Ultimately, there’s no one correct level of stringency. Programs may decide based on their policy objectives. For instance, if a program prioritizes environmental integrity, it might opt for stringent additionality rules. However, if the goal is to maximize participation and ensure an active market for GHG reduction credits, they might choose less strict rules to avoid rejecting projects that are actually additional. It’s about finding the right balance based on the program’s goals and priorities.

Selection of Baseline Procedures

Under the Project Protocol, there are two ways to estimate baseline emissions: the project-specific procedure and the performance standard procedure.

- Project-Specific Procedure:

This method tailors the baseline estimation specifically to each project. It involves looking at the project’s unique characteristics and determining what emissions would have occurred without the project’s activities.

- Performance Standard Procedure:

This approach sets a standard based on the average emissions of similar activities or technologies. The project’s emissions are then compared to this standard to estimate the reductions.The choice between these procedures impacts GHG project accounting because they can lead to different quantified GHG reductions for the same project.

As their names suggest, these procedures are linked to approaches for dealing with “additionality,” which is the idea that the emissions reductions claimed by a project should be additional to what would have happened without the project.

Why the choice matters:

- The decision on which procedure to use is crucial for addressing concerns about additionality in GHG programs.

- Additionally, practical matters come into play. GHG programs may prefer one procedure over the other for administrative reasons.

Administrative considerations:

- For instance, choosing the project-specific procedure might mean less preparatory work when starting a GHG program (although it might require more administrative work later on).

- On the other hand, developing performance standards may require a significant initial investment of resources, but it could lead to lower transaction costs once the GHG program is running.

From the perspective of a GHG program, policy considerations play a key role in deciding which baseline procedure project developers should use.

Secondary Effects Accounting

- Secondary Effects and GHG Emissions:

If a project has a secondary effect that leads to a significant increase in greenhouse gas (GHG) emissions, it can undermine or even cancel out the primary positive impact of the project.

- Need for Examining Secondary Effects:

To accurately measure the GHG reductions caused by a project, we need to look at its secondary effects. However, the challenge is figuring out how deep into these effects we should examine.

- Questions to Address:

- Breadth Question: How far should we go in examining secondary effects? For example, in a full “life cycle analysis” of GHG emissions for a product, we could look not just at the product itself but also at the emissions from the inputs to the product, the inputs to those inputs, and so on.

- Significance Question: How important are these secondary effects? In many cases, the secondary effects might be relatively small, especially for smaller projects. Yet, it takes time and money to estimate, monitor, and quantify these effects.

- Breadth Question: How far should we go in examining secondary effects? For example, in a full “life cycle analysis” of GHG emissions for a product, we could look not just at the product itself but also at the emissions from the inputs to the product, the inputs to those inputs, and so on.

- Tradeoff in GHG Project Accounting:

GHG project accounting involves deciding the tradeoff between accounting for secondary effects and the time and effort required to do so. - Policy Decisions for GHG Programs:

- From the perspective of GHG programs, deciding how extensively to account for secondary effects is a policy decision.

- Requiring a thorough and detailed accounting of secondary effects can ensure environmental integrity, meaning the environmental benefits claimed are accurate. However, it might discourage project participation because the requirements could be too burdensome for some developers.

- Strict requirements could also increase administrative costs needed to evaluate or verify these secondary effects.

- From the perspective of GHG programs, deciding how extensively to account for secondary effects is a policy decision.

Valid Time Length for Baseline Scenarios

- Valid Time Length for Baseline Scenarios or Performance Standards:

When setting up a baseline scenario or performance standard for a project, you need to decide how long it should be considered valid. This means determining the period during which the baseline or standard is relevant.

- Technical Considerations:

Technical factors, like advancements in technology and economic trends, can help guide the decision on how long a baseline scenario or performance standard should be. For instance, certain project types in a specific area might have a recommended time length based on these factors.

- Cumbersome Decision-Making for Individual Projects:

However, for greenhouse gas (GHG) programs, deciding on different valid time lengths for each project activity could be complicated and burdensome.

- Administrative Ease and Consistency:

- For practical and administrative reasons, it’s often simpler to adopt a common valid time length for all baseline scenarios or performance standards. This common period is typically several years.

- This approach helps provide consistent expectations for project developers. It means everyone is working with the same timeframe, making it easier to manage and understand.

- For practical and administrative reasons, it’s often simpler to adopt a common valid time length for all baseline scenarios or performance standards. This common period is typically several years.

- Administrative and Policy Considerations:

- When it comes to GHG programs, the main deciding factors in determining how long baseline scenarios or performance standards will be valid are administrative and policy considerations.

- These considerations include making things manageable from an administrative standpoint and aligning with the overall goals and policies of the program.

- When it comes to GHG programs, the main deciding factors in determining how long baseline scenarios or performance standards will be valid are administrative and policy considerations.

Static Versus Dynamic Baseline Emission Estimates

- Static vs. Dynamic Baseline Emission Estimates:

When setting up a baseline for greenhouse gas (GHG) emissions in a program, you need to decide whether to use static or dynamic estimates. - Tradeoff between Environmental Integrity and Program Participation:

From the perspective of a GHG program’s policies, the main issue in making this choice involves finding a balance between two important factors: environmental integrity and program participation. - Dynamic Baseline Emission Estimates:

Dynamic estimates are those that change to stay accurate and aligned with evolving circumstances. This ensures a higher level of environmental integrity because the estimates stay up-to-date. - Tradeoff Explanation:

The tradeoff comes in when considering the potential drawbacks of dynamic estimates:

- Increased Transaction Costs: Dynamic estimates might lead to higher transaction costs under a GHG program. This means more resources and efforts may be needed to manage and update these constantly changing estimates.

- Increased Uncertainty for Project Developers: Dynamic estimates introduce more uncertainty for developers participating in the program. This uncertainty can make it harder for them to plan and execute their projects.

- Potential Discouragement: The combination of higher transaction costs and increased uncertainty might discourage investments and limit the number of projects participating in the GHG program.

- Increased Transaction Costs: Dynamic estimates might lead to higher transaction costs under a GHG program. This means more resources and efforts may be needed to manage and update these constantly changing estimates.

- Finding the Right Balance:

GHG programs need to strike a balance between maintaining environmental integrity and encouraging project participation. Choosing dynamic baseline estimates can enhance accuracy but might come at the cost of increased complexity and uncertainty.